Description

The Global Agriculture Sensors Market size was USD 1.65 billion in 2022 and it is expected to grow to USD 4.13 billion in 2030 with a CAGR of 9.75% in the 2023-2030 period.

Global Agriculture Sensors Market: Overview

Agriculture sensors are called active sensors because they emit their light source onto the plant canopy and at the same time measure the percentage of light that is reflected from the canopy toward the sensor. Precision farming, also known as smart farming, allows farmers to maximize their yields with minimal resources. These sensors help understand plants at the microscale to conserve resources and reduce environmental pollution. Many sensor technologies are implemented in precision agriculture and provide data to help farmers monitor and optimize crop yield.

Agriculture sensors are enjoying increasing popularity among farmers due to the increasing need for optimal production with the resources provided. Additionally, changing weather patterns due to increased global warming have required advanced sensors to increase productivity and crop yields. By offering advanced sensors, farmers can monitor farms, and weather forecasts, and achieve optimal field requirements. Agriculture sensors allow farmers to increase yields with minimal human effort and waste.

Global Agriculture Sensors Market: Covid-19 Impact

The pandemic led to disruptions in global supply chains, including the production and distribution of agriculture sensors. Manufacturing facilities faced temporary closures, delayed shipments, and shortages of raw materials, affecting the availability of sensors in the market. During the early stages of the pandemic, many regions implemented lockdowns and restrictions that impacted agricultural activities. Farmers faced labor shortages, transportation challenges, and limited access to markets, leading to a decline in the adoption of new technologies, including agriculture sensors. The economic impact of the pandemic affected farmers’ budgets and investment decisions. Many farmers had to prioritize essential expenses and postpone investments in technologies like agriculture sensors, which are often considered long-term investments. The pandemic also brought about changes in consumer behavior and preferences, leading to shifts in agricultural production. For example, there was an increased demand for certain crops like fruits and vegetables, while the demand for non-essential crops may have declined. This shift in production patterns could influence the demand for specific types of agriculture sensors.

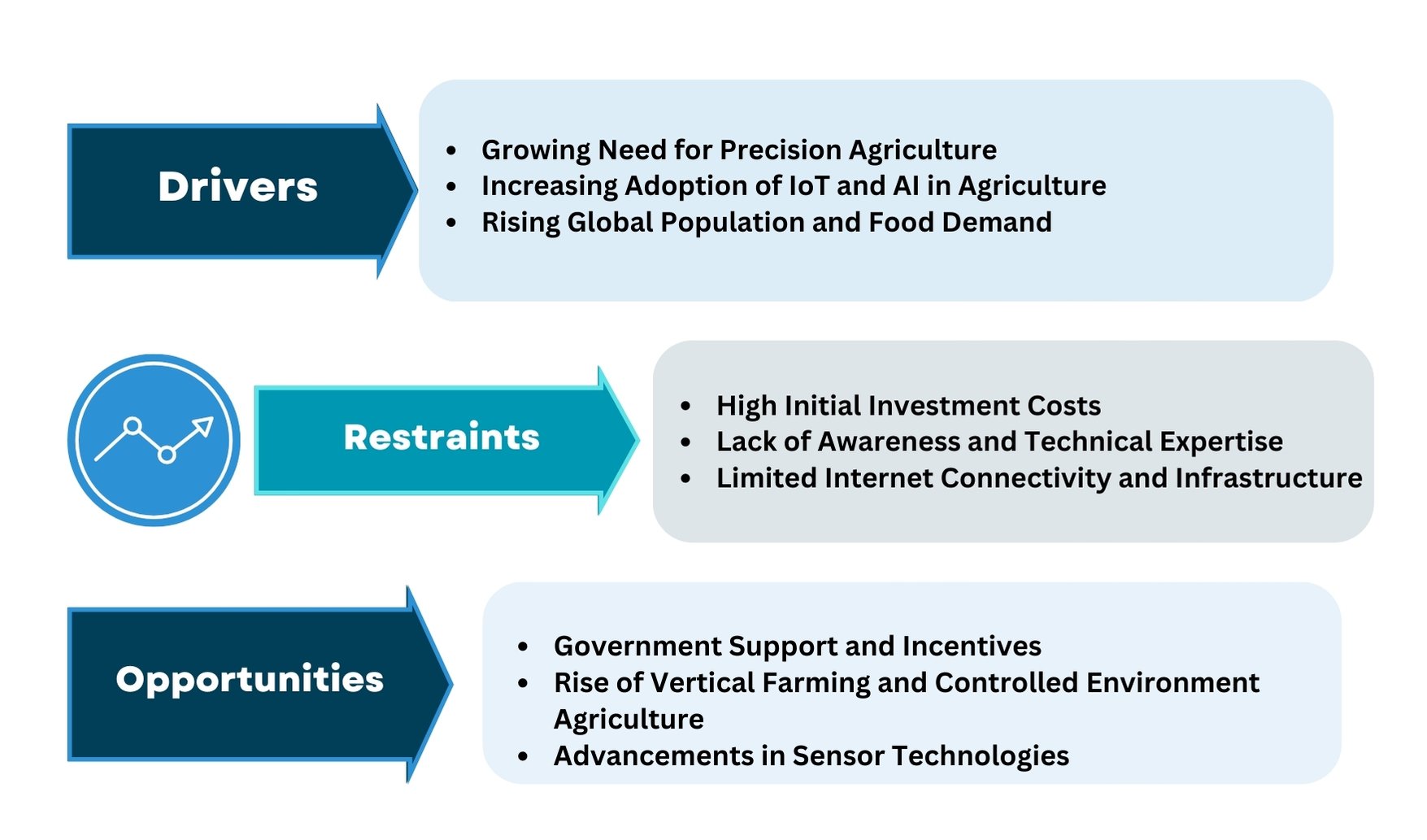

Global Agriculture Sensors Market: Growth Drivers

-

Growing Need for Precision Agriculture:

Precision agriculture involves the use of advanced technologies to optimize farm management practices. Agriculture sensors play a crucial role in this domain by providing real-time data on soil conditions, weather patterns, crop health, and other variables. Farmers are increasingly adopting precision agriculture techniques to improve crop yields, reduce resource wastage, and enhance overall efficiency.

-

Increasing Adoption of IoT and AI in Agriculture:

The Internet of Things (IoT) and Artificial Intelligence (AI) have gained prominence in the agriculture sector. Agriculture sensors, when integrated with IoT and AI platforms, enable smart farming practices. These technologies empower farmers to monitor and control their agricultural operations remotely, leading to better decision-making and resource management.

-

Rising Global Population and Food Demand:

With the world’s population steadily increasing, the demand for food is also rising. Agriculture sensors help farmers increase productivity and optimize resource usage, which is crucial to meet the growing food demand sustainably.

Global Agriculture Sensors Market: Restraining factors

-

High Initial Investment Costs:

The upfront costs of purchasing and implementing agriculture sensor technologies can be a significant barrier, especially for small-scale farmers or those operating in developing regions. The high initial investment may discourage some farmers from adopting these technologies, even though they offer long-term benefits.

-

Lack of Awareness and Technical Expertise:

Many farmers, particularly in rural areas, may not be familiar with the potential benefits of agriculture sensors or lack the technical expertise to operate and integrate these technologies effectively. The lack of awareness and training could limit their adoption and utilization.

-

Interoperability and Data Standardization Challenges:

As the agriculture sector embraces various sensor technologies, there might be compatibility and data standardization issues. Different sensors may generate data in various formats, making it challenging to integrate and analyze information effectively. This lack of interoperability can be a barrier to seamless sensor deployment.

-

Limited Internet Connectivity and Infrastructure:

In some remote or rural agricultural regions, access to high-speed internet connectivity and robust infrastructure may be limited. Agriculture sensors often rely on internet connectivity for real-time data transmission and remote monitoring, making their implementation challenging in areas with poor network coverage.

Global Agriculture Sensors Market: Opportunity Factors

-

Government Support and Incentives:

Governments in various countries have been promoting the adoption of modern agricultural technologies, including agriculture sensors. Supportive policies, financial incentives, and subsidies for farmers have encouraged the uptake of these technologies.

-

Need for Water Conservation and Efficient Irrigation:

Water scarcity is a significant challenge in many regions worldwide. Agriculture sensors assist in measuring soil moisture levels and crop water requirements, enabling efficient irrigation practices and water conservation.

-

Rise of Vertical Farming and Controlled Environment Agriculture:

Vertical farming and controlled environment agriculture are innovative approaches to cultivation that rely heavily on technology, including agriculture sensors, to create optimal growing conditions. These practices are gaining popularity due to their potential for year-round production, reduced land use, and higher crop yields.

-

Advancements in Sensor Technologies:

Technological advancements have led to the development of more sophisticated and affordable agriculture sensors. As the cost of these sensors decreases and their capabilities improve, their adoption becomes more feasible for a broader range of farmers and agricultural operations.

Global Agriculture Sensors Market: Challenges

-

Complexity and Calibration:

Some agriculture sensors require regular calibration and maintenance to ensure accurate and reliable data collection. The complexity of these processes and the need for periodic calibration may pose challenges for some farmers.

-

Environmental and Ethical Concerns:

Certain sensor technologies may raise environmental or ethical concerns, such as the environmental impact of sensor components or the use of data for unintended purposes. Addressing these concerns and ensuring sustainable and responsible use of agriculture sensors is essential.

-

Regional Variations and Adaptability:

Agriculture practices vary significantly across regions and climates. Agriculture sensors should be adaptable to different farming practices and environmental conditions to provide meaningful insights and value to farmers worldwide.

-

Market Fragmentation:

The agriculture sensors market can be fragmented with a wide range of sensor types and technologies available. This fragmentation can lead to confusion among farmers and decision-makers about which sensors best suit their specific needs.

Global Agriculture Sensors Market: Segmentation

Based on Type: The market is segmented into Location Sensors, Humidity Sensors, Electrochemical Sensors, Mechanical Sensors, Airflow Sensors, Pressure Sensors, Optical Sensors, Water Sensors, Soil Moisture Sensors, and Livestock Sensors depending on the type segmentation. Among these, the location sensor segment dominates the market.

Based on Application: Based on application segmentation, the market is further divided into Dairy Management, Soil Management, Climate Management, Water Management, Smart Green House, and Others. Among these, the soil management application segment dominated the market.

Based on Region: Based on Region, the market is segmented into five key geographical regions namely – North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Global Agriculture Sensors Market: Regional Insights

The global Agriculture Sensors market is geographically segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Each region has its own market dynamics and demand drivers, which can influence the revenue contribution and growth opportunities in the Agriculture Sensors market. North America dominated the market. The dominance can be credited mainly to the relatively greater adoption of sensors across the agriculture segments. The U.S. is house to a large number of soil moisture sensor manufacturers such as Sensaphone, Sentera, Texas Instruments Incorporated, and Monnit Corporation. Stringent environmental regulations and the rising adoption of precision farming and yield monitoring practices by large and small farm owners to upsurge the productivity of fields are expected to drive the market.

Asia Pacific region is estimated to register the highest CAGR during the forecast period owing to increasing awareness regarding the usage of soil moisture sensors among farmers. Furthermore, the availability of vast agricultural lands in countries such as China and India is expected to increase the use of soil moisture sensors. The increasing concern for soil health in the region is having a positive impact on market growth. Countries such as India, Japan, China, and Australia, are expected to generate substantial revenue due to favorable government policies and increasing disposable income of farmers.

Global Agriculture Sensors Market: Competitive Analysis

The Global Agriculture Sensors Market is driven by various key players such as auroras Srl Cso Piera Cillario, Caipos GmbH, CropIn Technology Solutions Private Limited, CropX inc., dol-sensors A/S, Glana Sensors AB, Libelium Comunicaciones Distribuidas S.L., Monnit Corporation, pycno agriculture, Sensaphone.

Global Agriculture Sensors Market: Recent Developments

- January 2023: CropX Technologies, a global leader in digital solutions for agronomic farm management, acquired Tule Technologies, a precision irrigation company based in California. This acquisition brings new data capture technologies to the CropX Agronomic Farm Management System and expands its market in California drip-irrigated specialty crops.

- October 2022: Reinke Irrigation, a leading center pivot manufacturer, partnered with CropX Technologies, the developer of a digital agronomic farm management platform to ensure the optimization of water use in crop production and maximizing crop production.

- August 2022: CropX Technologies launched continuous nitrogen leaching monitoring capability. It is easier, less time-consuming, and able to supply continuous monitoring of nitrogen leaching events than traditional lab testing methods.